In 1995 I moved from Paris to London. As exciting and interesting that London was and is, I was keen to keep up with what was going on in France. Back then trying to follow French media was extremely hard.

TV was a non-starter, radio – no chance and the internet was pretty basic. Most newspapers did not have an online presence which meant having to trek to specialist newsagents in South Kensington to get a copy of Le Figaro or le Monde. Twenty years later it’s all in available in 5.5-inch device in my pocket, and now in “Technicolor”.

So what! The so what is that it’s easy to forget just how far we have come in such a short period of time. Ubiquitous new technology and telecom infrastructures have been built to make this happen and now with 5G networks at our door, the telco industry embarks on the next major investment to enable me to watch Gerard Depardieu on TV5 anywhere I wish. The energy consumption to support this next wave, if unchecked, has the potential to derail the financial benefits of that investment.

Energy in 3D

Our experiential age future is built on energy and connectivity!

Big Data will drive the 4th Industrial Revolution and energy shall be her engine. And with most great things, they come at a price. Connectivity is extremely hungry for energy. As connectivity increases, so too does energy consumption.

The business case for the operator will be squeezed between the two: the idyllic world of mass wireless connectivity and the enormous energy force required to realise it.

Energy cost reduction is essential for successful business case

The telecom networks’ critical infrastructure has a trio of challenges:

De-Centralisation – Maintaining telecom network reliability while critical functions are pushed closer towards the end user. Network functions are being removed from their centralised, maintained locations and being re-located within the served community itself, where they are less physically secure and far more vulnerable to the forces of nature. Streaming HD video being the most visible application of this right now – the end user will not tolerate latency issues, therefore for both user experience reasons and also cost for the provider they need to get the content closer to the user.

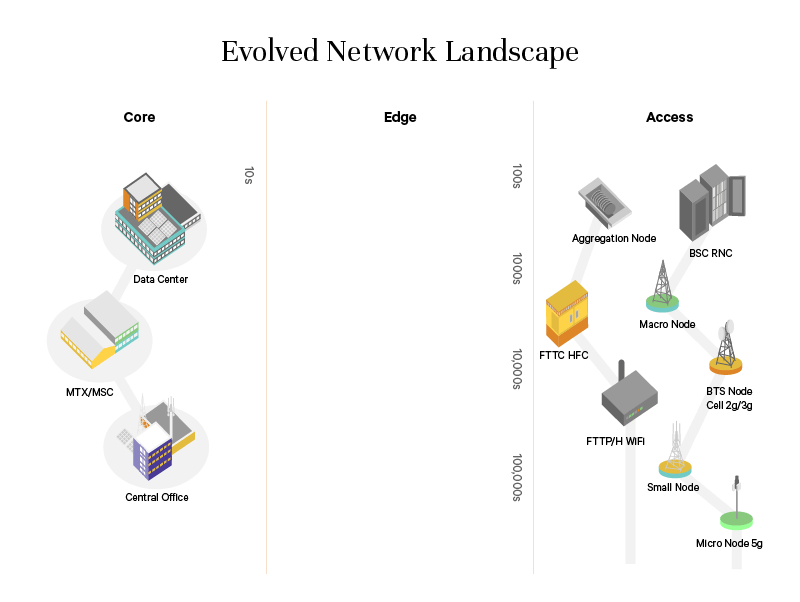

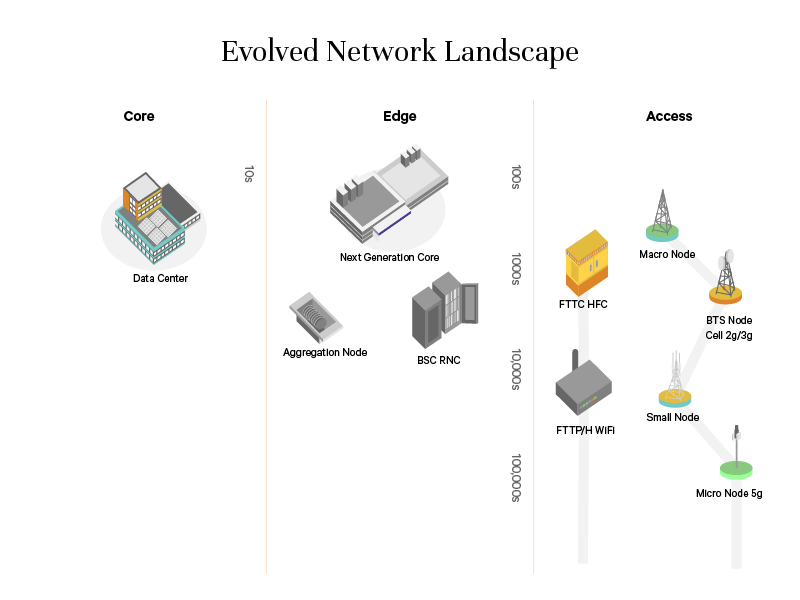

The two charts illustrate this new Edge network landscape evolution with 5G infrastructure.

Before

After

De-carbonisation – Energy consumption is being transferred from the physical to a digital environment (movement of goods, services, people changing to a new economic environment). The positive of this is that the evolved telecom network will reduce the carbon burden on the end user. However, because the network has to reach more places and in greater strength to achieve that, it will require a considerable increase in energy consumption.

The recent SMARTer 2030 report produced by Accenture for GeSI projected that, despite the expected growth of the ICT sector, which includes mobile operators, the relative carbon footprint is anticipated to remain around 2 percent of total global emissions as far ahead as 2030. More importantly, the future carbon emissions abatement potential of the ICT sector as a whole, including mobile, was estimated at 20 percent of global CO2e emissions by 2030.

Notwithstanding, as I write this blog up to 70,000 schoolchildren each week in 500 towns and cities worldwide are striking over climate change. I suspect the irony that this generation are the most digital-information hungry of all has been lost on them. However, what it shows is that pressure to reduce the reliance of traditional energy sources, use cleaner, more sustainable energy, like replacing local diesel generation and oil / gas driven utility production will not only increase but are also in many of the CSR statements of the operators. How the operator performs is likely to become a strong factor in brand choice for this generation.

Digitalisation – Making the energy infrastructure benefit from the enhanced network in terms of efficiency – things you could no longer see you now can under the energy realm. Ability to see the network ecosystem include energy as one of its functions, not as a necessary evil to support the functions.

Energy reigns sovereign

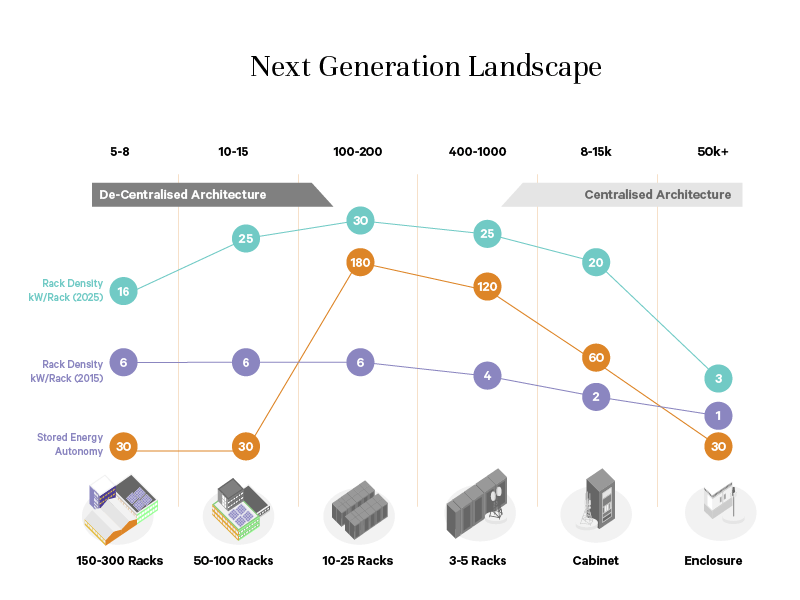

Intelligent connectivity has highest consumption impact in Node and Macro. Density in data centre increases sees 3rd highest increase.

Increased energy consumption by network area.

In terms of the critical infrastructure requirements, we can split this down to see where the impact is happening on power and cooling.

We see de-centralised architecture coming from the core and centralised architecture coming from access. Densification is having a heavy impact across the landscape through asset concentration in terms of the need for energy being used in cooling.

And because only about 15% of sites have a diesel generator at the edge, battery autonomy at these sites soars hence we see a spike in requirement in that area. (below)

Critical edge sites will require significant back up resilience.

Consorting with Allies

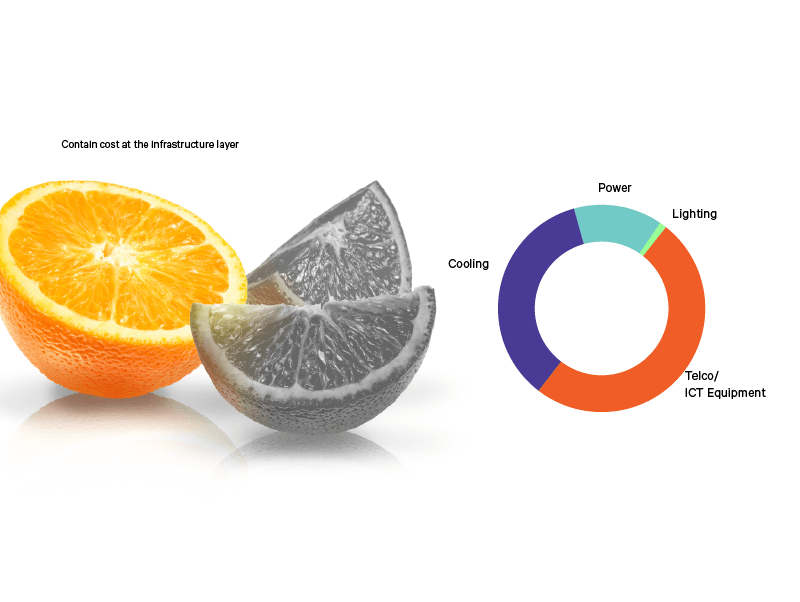

If you view the operators cost buckets simplistically as a 4-segment orange (below image), you have:

Segment 1: Reduce Utility energy costs – Bill challenging. New PPA agreements – done.

Segment 2: Contain costs in service applications – efficient radio and core applications – done

The remaining two segments are the costs addressing the consumption behind the utility meter.

This is especially challenging as the telecom network is evolving at the same time efficiencies are being made.

King’s ransom or Princely sum?

Containing and reducing costs at the infrastructure layer can be addressed in more than one way. Our experience working with operators is that starting from the point of understanding what best practice actually looks like is fundamental to understanding how to emulate it.

Exchanging physical components will certainly help but it is likely to be a more incremental and piecemeal route.

If something cannot be measured, it cannot be improved. Site auditing and measurement is a more holistic approach. Performance visualisation tools mine the data and present palatable, real-time analysis of consumption and performance. Interpreting the findings correctly is therefore key to a positive outcome. This requires the support of companies who understand how to interpret and recommend courses of actions.

If CapEx budgets are constrained, there are other options. Disruptive business models such as ESaaS (energy savings as service pioneered by Vertiv) have proven to combat the expected infrastructure needs.

Abdication not an option

Profound changes to our lives should mirror the profound changes to the networks.

Power is the commodity that shapes Digitalisation and De-Centralisation. De-Carbonisation and Efficiency are shaped by knowledge.

Knowledge is Power.

Knowledge of Power is Efficiency.

Feel free to subscribe to our blog to stay informed on the latest trends, technologies and news.